You’ve probably heard it before: Don’t put all your eggs in one basket.

It’s old advice — maybe too old. But in investing, it’s never stopped being true.

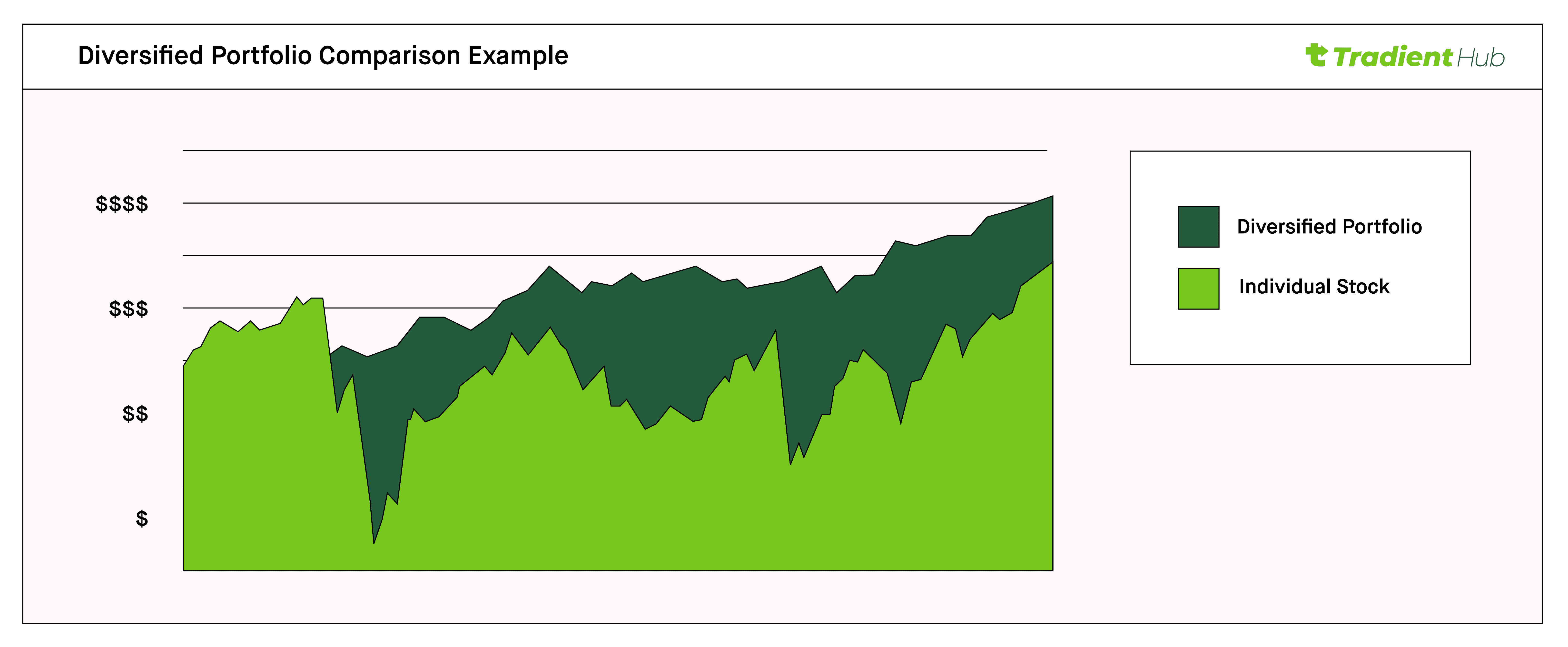

A diversified portfolio is the modern version of that proverb, only the baskets now include tech stocks, treasury bonds, foreign currencies, and maybe even a REIT or two. The principle, though, hasn’t changed: when one basket tips, you don’t lose everything.

Why Diversification Still Matters

Imagine your finances as a house built on several pillars.

If one cracks — say, the stock market tumbles — the others, like bonds or cash reserves, keep the house standing. The idea isn’t to make your portfolio invincible; it’s to make it resilient.

In essence, diversification helps you manage the unpredictable. It’s not about chasing every opportunity; it’s about not being cornered by any single mistake. You’re reducing the chance that everything goes wrong at once.

Or as one old fund manager once told me, “Diversification doesn’t make you rich fast — it keeps you from getting poor fast.”

A Better Way to Picture It

Think of your investments like a well-balanced meal.

Your portfolio needs its proteins (stocks that drive growth), its carbs (bonds and cash equivalents that keep energy steady), and a few micronutrients — maybe commodities, real estate, or even alternative assets for that extra resilience.

Too much of one food group? You’ll feel great for a while — until you burn out.

Too little of another? You’ll never reach your full potential.

That’s diversification in a nutshell: not about perfection, but about balance that endures over time.

What Does a Diversified Portfolio Actually Look Like?

Diversification happens on several levels:

Across asset classes: stocks, bonds, real estate, cash, commodities.

Within each asset class: different companies, sectors, and sizes — from scrappy startups to global giants.

Across regions: the U.S., Europe, Asia, emerging markets.

Across currencies and time horizons: because the world doesn’t move in sync.

When the tech market in the U.S. hits turbulence, perhaps energy stocks or foreign bonds hold steady.

When one country’s economy contracts, another might quietly thrive.

That’s the quiet genius of diversification: your portfolio hums along even when one instrument plays off-key.

So, What’s Your Right Mix?

That depends on who you are. Investing isn’t just about spreadsheets and forecasts — it’s also about personality.

Ask yourself three things:

Why are you investing?

Maybe you’re building an emergency fund, paying down student loans, or saving for retirement. Your “why” defines how long your money can stay invested and how much risk it can stomach.

How do you handle risk — really?

Everyone says they can handle volatility until their portfolio drops 15%. If you lose sleep when markets swing, you might lean toward more stable assets. If you can stomach the ride, a heavier stock allocation could reward you over time.

3.What’s your timeline?

The longer your runway, the more risk you can afford. Time has a way of smoothing volatility — it’s why retirement accounts can handle more ups and downs than short-term savings.

There’s no universal formula. A 25-year-old freelancer saving for retirement and a 50-year-old business owner nearing college tuition payments shouldn’t own the same portfolio. The right mix is the one that lets you stay invested through uncertainty.

The Major Players: Three Core Asset Classes

Let’s ground this in the basics.

Stocks: High risk, high potential. They can surge 30% in one year — or sink just as fast. They’re the engines of growth but require patience and grit.

Bonds: The steady heartbeat of most portfolios. They generally offer smaller but more predictable returns and can cushion the blow when stocks stumble.

Cash and cash equivalents: The comfort zone — safe, accessible, and low-yielding. Great for short-term needs or parking funds when the world feels shaky.

Beyond those, there’s a universe of other options — real estate, gold, commodities, even private equity. Each comes with its own rhythm, its own season of strength and weakness.

Why All This Balancing Act Matters

Here’s the trade-off: concentration can make you rich, but diversification helps you stay rich.

Put 100% of your money into one company or one country, and your future depends on forces you can’t control — an earnings miss, a policy shift, or just bad luck. Spread it out thoughtfully, and one market’s slump can be softened by another’s rally.

Markets move in cycles. The trick isn’t to predict the next one — it’s to make sure your portfolio can survive whichever comes first.

Getting Help (Without Losing Control)

If the idea of building your own diversified portfolio sounds intimidating, you’re not alone.

That’s why mutual funds and exchange-traded funds (ETFs) exist — they’re like curated playlists built by professionals who do the balancing for you.

You can also work with a financial advisor who tailors a plan to your goals and temperament. Just remember: expertise comes at a price. Fees can quietly eat into returns, so choose partners who are transparent, not just persuasive.

In the end, you don’t need to do it all yourself — you just need to understand what you own and why.

The Hidden Trade-Offs

Diversification isn’t perfect.

It won’t prevent losses in a bear market, and it can sometimes dampen gains in a bull one.

When everything’s booming, a portfolio filled with only the winners might outshine yours.

But that’s the point — your goal isn’t to win every single year.

It’s to stay in the game every year.

Think of diversification as the difference between sprinting and distance running.

The sprinter might look glorious in the short term, but the marathoner — the steady, balanced investor — usually crosses the finish line first.

The Takeaway

A diversified portfolio won’t promise endless gains or guarantee safety.

What it offers is something rarer in investing: peace of mind.

It helps you build a future that can weather bad headlines, economic cycles, and the occasional panic on Wall Street.

Because when you spread your bets intelligently — across assets, across time, across continents — you’re not just diversifying your money.

You’re diversifying your future possibilities.

Final Note:

Diversification doesn’t ensure a profit or eliminate risk — but it gives you something far more practical: the ability to stay invested through uncertainty.

And that, over a lifetime, is what tends to matter most.

Disclaimer:

This presentation is for informational and educational use only and is not a recommendation or endorsement of any particular investment or investment strategy. Investment information provided in this content is general in nature, strictly for illustrative purposes, and may not be appropriate for all investors. It is provided without respect to individual investors’ financial sophistication, financial situation, investment objectives, investing time horizon, or risk tolerance. You should consider the appropriateness of this information having regard to your relevant personal circumstances before making any investment decisions. Past investment performance does not indicate or guarantee future success. Returns will vary, and all investments carry risks, including loss of principal. Tradient makes no representation or warranty as to its adequacy, completeness, accuracy or timeline for any particular purpose of the above content.